- Retail Banking and Consumer Lending

- Commercial Banking and Corporate Finance

- Capital Markets and Investment Management

- Insurance

- Payments, Fintech, and Digital Assets

- Cross-Cutting: Risk, Compliance, and Operations

- Deployment Considerations for Financial Services

- Why Financial Institutions Choose Space-O AI

- Frequently Asked Questions

20 Generative AI Use Cases in Financial Services for Banking, Insurance, and Capital Markets

Generative AI does two things that earlier AI could not. It reads and produces unstructured content at scale (contracts, filings, emails, advisor notes, claims documentation), and it holds a coherent conversation with customers and employees. Almost every high-value generative AI use case in financial services builds on those two capabilities. 76 percent of insurers have already implemented generative AI in insurance in one or more business functions, with life and annuity carriers slightly ahead of property and casualty insurers.

The bar for getting it right is higher here than in any other industry. Models that touch credit decisions, customer interactions, or trading systems sit under governance and oversight requirements that horizontal templates were not built for.

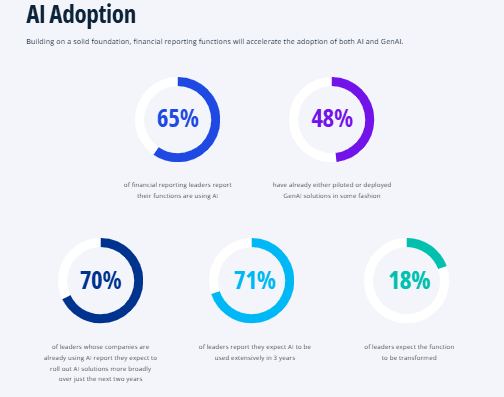

Adoption is accelerating anyway. Based on findings from KPMG, 65 percent of financial reporting leaders are using AI in their workflows, 48 percent have piloted or deployed GenAI, and 71 percent expect AI to be used extensively within three years.

Space-O AI builds custom generative AI for financial institutions that need production-grade software meeting institutional governance, security, and compliance requirements. Our generative AI development services and AI for finance solutions cover the use cases below as deployable applications.

This guide covers 20 generative AI use cases organised by subsector: retail banking and consumer lending, commercial banking and corporate finance, capital markets and investment management, insurance, payments and fintech, and a cross-cutting layer on risk, compliance, and operations.

Retail Banking and Consumer Lending

Retail banking is where generative AI meets the customer at scale. Call volume is high, queries are repetitive, and the cost of getting it wrong is direct: a wrong fee disclosure, a missed adverse action notice, or an inconsistent product recommendation can trigger consumer protection exposure.

According to EY-Parthenon’s 2025 Generative AI in Banking survey, 77 percent of banks have now actively launched or soft-launched GenAI applications, up from 61 percent in 2023, with 89 percent expecting major transformative benefits within the next two years. The four use cases below are where most retail banks are now actively deploying in production.

| # | Use Case | Core Problem | Technical Approach | Who It’s For |

|---|---|---|---|---|

| 1 | Conversational customer service and self-service banking | Repetitive high-volume queries, limited self-service | LLM assistant with retrieval and tool-use APIs | Retail banks, neobanks, credit unions |

| 2 | Credit decisioning support and adverse action notices | Manual notice drafting, fair-lending compliance | LLM-generated explanations from decision factors | Consumer lenders, card issuers |

| 3 | Personalized financial advice and product recommendations | Untapped customer data, generic messaging | Generative personalization with segmentation logic | Retail banks, savings and wealth platforms |

| 4 | Mortgage and loan document processing | Document-heavy origination workflow | LLM classification and extraction on loan documents | Mortgage lenders, consumer loan originators |

1. Conversational customer service and self-service banking

What it is: A modern banking assistant that reads the customer’s account context in real time, understands queries phrased in natural language across multiple turns, and resolves the request end-to-end (initiating a dispute, ordering a replacement card, explaining a specific charge) by calling backend systems via API.

How generative AI enables it: Routine queries (balance, transactions, lost cards, dispute status, fee questions) absorb 60 to 70 percent of agent time. The new generation of assistants handles them autonomously by combining a language model with a retrieval layer over policy documents, fee schedules, and product terms, plus tool-use integrations into core banking, card management, and fraud systems.

Key capabilities:

- Resolves account-level requests end-to-end (dispute initiation, card replacement, fee explanation) without human escalation, built on a custom LLM development stack

- Understands natural-language queries across multiple turns and remembers context within the conversation

- Hands over to a human agent with the full conversation context so the customer does not have to repeat themselves

- Stays bounded: cannot speculate about markets, cannot infer eligibility for products the customer has not requested, cannot recommend competitive products

Business impact: Contact centre costs are among the largest controllable expenses in retail banking. Deflecting routine queries from human agents to an AI assistant compresses cost per interaction while raising customer satisfaction on the same volume.

Who it’s for: Retail banks, neobanks, credit unions, and any consumer financial institution where call volume is the primary cost driver and self-service has historically been weak.

2. Credit decisioning support and adverse action notice generation

What it is: Generative AI drafts the adverse action notices required under U.S. fair-lending rules when a bank denies credit, applies the bank’s preferred language conventions, and produces a customer-readable explanation that satisfies regulatory requirements without manual review on every case.

How generative AI enables it: Credit decisioning has been algorithmic for decades. What generative AI adds is the explanation layer. The model reads the underlying decision factors, generates the customer-facing notice in compliant language, and surfaces the supporting documentation. The decision itself stays with the credit policy and the underwriter.

Key capabilities:

- Generates adverse action notices at scale with consistent, compliant language based on the underlying decision factors

- Supports credit analysts on judgment-based decisions by summarising the application, flagging missing information, and surfacing comparable prior decisions

- Provides a full audit trail linking each notice back to the decision factors that produced it

- Operates as a productivity layer on top of the existing decisioning framework, in line with AI in risk management practices

Business impact: Adverse action notices are a high-volume regulatory deliverable that historically required manual review. AI reduces the per-notice cost while improving consistency, which lowers regulatory exposure and frees credit analysts for judgment-intensive work.

Who it’s for: Consumer lenders, credit card issuers, auto lenders, and any institution operating under U.S. fair-lending rules at meaningful application volume.

3. Personalized financial advice and product recommendations

What it is: A personalization engine that drafts targeted in-app messages, email content, and product recommendations tied to each customer’s actual behaviour: a customer who started receiving a larger paycheque is a candidate for a savings product conversation; a customer with consistent international transactions is a candidate for a multi-currency account.

How generative AI enables it: Most retail banks have customer data they cannot meaningfully act on. Transaction history, savings patterns, life-stage signals, and product holdings sit in separate systems that no relationship manager has time to correlate manually. Generative AI changes that economics by drafting the communication at scale while the bank retains the segmentation logic, product eligibility rules, and required disclaimers.

Key capabilities:

- Generates targeted customer communications tied to actual behaviour rather than segment averages

- Respects every opt-out, do-not-contact, and channel preference in the bank’s preference centre

- Produces an audit trail for each communication so every message is reviewable on demand

- Applies the bank’s regulatory disclaimers consistently across messages and channels

Business impact: Personalised communications materially outperform generic outreach on engagement and conversion. The compound effect across the customer base shows up in product attachment, deposit growth, and customer retention.

Who it’s for: Retail banks, savings platforms, wealth and advisory platforms with retail tiers, and any institution where customer data sits underutilised.

4. Mortgage and loan document processing

What it is: Generative AI compresses the document handling layer of mortgage and consumer loan origination. It classifies each document on intake, extracts key data into the loan origination system, flags inconsistencies, and drafts the underwriter’s summary.

How generative AI enables it: A single mortgage application generates dozens of documents (income verification, tax returns, appraisals, title reports, insurance certificates, employment letters) that need to be read, classified, validated, and routed through underwriting in a way that meets investor and regulatory documentation requirements. The model handles the classification and extraction layer; the underwriter still owns the decision.

Key capabilities:

- Classifies incoming documents and routes them to the right step in the origination workflow

- Extracts structured data (income figures, addresses, employment history) and populates the loan origination system

- Flags inconsistencies (income on the W-2 versus the application, address mismatches, missing pages) before the file reaches underwriting

- Drafts the underwriter’s summary so reviewers focus on judgment, not file assembly

Business impact: Origination cycle time is one of the largest competitive differentiators in mortgage lending. The parallel build pattern is well-established: our AI document analyzer case study shows the architecture of a custom system built for structured extraction across complex document types, with the same principles transferring directly to mortgage and consumer loan origination.

Who it’s for: Mortgage lenders, consumer loan originators, and any institution running document-heavy origination at meaningful volume.

Commercial Banking and Corporate Finance

Commercial banking lives in long-form documents. Credit memos, term sheets, supporting financials, KYC files, customer correspondence. The relationship manager spends a meaningful share of every week on documentation rather than relationship building, which is where generative AI delivers measurable hours back to the front-line team.

McKinsey’s analysis of generative AI in banking estimates that gen AI could deliver $200 billion to $340 billion in annual value across the global banking sector, with corporate banking sitting among the largest absolute opportunities.

| # | Use Case | Core Problem | Technical Approach | Who It’s For |

|---|---|---|---|---|

| 5 | Credit memo drafting and underwriting support | Long memo drafting cycles | LLM drafting on financials and research repository | Commercial banks, corporate lenders |

| 6 | Cash management and treasury services AI | Manual treasury inquiries | LLM assistant integrated with cash management platform | Corporate banks, treasury services providers |

| 7 | Relationship manager copilot for corporate banking | Fragmented customer data across systems | LLM copilot on CRM, transaction, and document systems | Corporate and commercial banks |

5. Credit memo drafting and underwriting support

What it is: Generative AI compresses the first-draft cycle of commercial credit memos from days to hours by reading the borrower’s financials, drafting the financial analysis section, summarising the borrower’s prior banking relationship, and producing a complete first draft that the analyst then refines.

How generative AI enables it: A commercial credit memo for a mid-market borrower can run 30 to 60 pages, drawing on financial statements, industry reports, customer interview notes, and internal credit policy. The model assembles the structured sections from existing data sources while the analyst retains the credit judgement and the final memo.

Key capabilities:

- Generates the financial analysis section directly from the borrower’s statements with consistent formatting

- Drafts the industry overview from the bank’s internal research repository

- Summarises the borrower’s prior banking relationship from CRM and transaction history

- Produces a structured first draft that the credit analyst refines rather than writing from a blank page

Business impact: McKinsey has documented examples of banks compressing investment-brief production from roughly nine hours to thirty minutes after deploying the model on top of internal data. At the volume of memos commercial banks produce annually, the compound effect on analyst capacity is significant.

Who it’s for: Commercial banks, corporate lenders, syndicated lending desks, and any institution running document-intensive credit underwriting.

6. Cash management and treasury services AI

What it is: A treasury services assistant that answers corporate treasurer queries (consolidated cash position, FX exposure, wire status) in plain language by reading the bank’s cash management platform via API and surfacing relevant data with citations to the source system.

How generative AI enables it: Corporate treasurers spend much of their time on inquiries that are essentially data retrieval, which has historically required either pulling reports manually or calling a relationship manager. A modern assistant resolves these queries autonomously while respecting the corporate hierarchy’s entitlement model.

Key capabilities:

- Answers cash position, FX exposure, and transaction status queries in plain language

- Respects the corporate hierarchy: each user only sees the accounts and entities they are entitled to

- Cites the source system for every answer so the treasurer can validate against the underlying record

- Integrates with the bank’s cash management platform via AI integration work covering the full API surface

Business impact: Treasurer self-service reduces relationship manager time spent on data lookups, freeing the RM for advisory conversations. Customer satisfaction improves on the same volume because answers arrive immediately rather than via callback.

Who it’s for: Corporate banks, treasury services providers, and any institution offering cash management to mid-market and large corporate customers.

7. Relationship manager copilot for corporate banking

What it is: A copilot that consolidates the corporate banking customer view across CRM, transaction systems, and document repositories. Before a meeting, it generates a briefing covering account history, recent transactions, outstanding service issues, recent earnings or news, and prior interactions across product specialists.

How generative AI enables it: The corporate banking RM is asked to be financial analyst, product specialist, account historian, and primary contact at once. Each role is documentation-heavy, and most of that documentation lives in systems that do not talk to each other. The copilot assembles the integrated view that the RM previously had to build manually for every interaction.

Key capabilities:

- Generates pre-meeting briefings covering account history, recent transactions, and prior product specialist interactions

- Transcribes and summarises the meeting, surfacing action items and follow-up points

- Drafts the follow-up email and the internal call report in the bank’s preferred conventions

- Connects to CRM, transaction systems, and document repositories via custom LLM development integration

Business impact: Front-line RM time is one of the highest-value resources in commercial banking. Reclaiming hours per RM per week from documentation and meeting prep translates directly into more customer conversations and higher revenue per RM.

Who it’s for: Corporate and commercial banks, syndicated lending teams, and any institution where the RM is a primary revenue driver.

Capital Markets and Investment Management

Capital markets ran on algorithms before consumer AI existed. The new wave automates the research and content layer that human analysts still hand-craft: reading earnings calls, summarising filings, drafting pitch books, synthesising trading desk research. Each one is a long-form content problem on top of a high-volume data environment.

| # | Use Case | Core Problem | Technical Approach | Who It’s For |

|---|---|---|---|---|

| 8 | Earnings call and 10-K analysis at scale | Coverage gaps on non-watchlist companies | LLM summarisation of filings and transcripts | Buy-side and sell-side research |

| 9 | Investment research assistant | Slow synthesis of internal and external research | RAG on research corpus | Asset managers, investment banks |

| 10 | Pitch book and investment memo generation | Manual assembly of standard sections | LLM drafting on deal databases and comps | Investment banks, M&A advisors |

| 11 | Trading desk research synthesis | Lag between event and synthesised briefing | Agentic monitoring and summarisation | Sales and trading desks |

8. Earnings call and 10-K analysis at scale

What it is: Generative AI reads every earnings call transcript and quarterly filing across a defined coverage universe and generates structured summaries covering guidance changes, sentiment shifts, key disclosures, and management tone, routed into the analyst’s preferred workflow.

How generative AI enables it: Coverage is selective at most research desks because the volume of filings and transcripts exceeds any team’s manual reading capacity. AI scales the reading and first-pass synthesis across the full universe, surfacing the signals worth the analyst’s attention.

Key capabilities:

- Reads every transcript and filing across the coverage universe at scale, not only the watchlist

- Generates structured summaries (guidance, sentiment, key disclosures, management tone) in consistent formats

- Surfaces material changes from prior quarters so analysts focus on what moved rather than re-reading what stayed the same

- Built on a retrieval-augmented generation stack tuned to the specific terminology of accounting and securities disclosures

Business impact: Coverage expands without adding headcount. The analyst’s time shifts from reading to interpretation, which is the higher-value step. Material signals in non-watchlist companies that previously went uncovered now reach the desk.

Who it’s for: Buy-side research teams, sell-side equity research, hedge funds, and any institutional investor with a defined coverage universe.

9. Investment research assistant

What it is: A research assistant that lets analysts query the firm’s full corpus of internal notes, broker research, regulatory filings, and macroeconomic data in natural language and returns synthesised answers with citations linking back to the source documents.

How generative AI enables it: Internal research notes from prior quarters become discoverable rather than stored. External sell-side research, regulatory filings, and macroeconomic context can be integrated alongside. The retrieval architecture controls hallucination by grounding answers in the firm’s authoritative content.

Key capabilities:

- Queries internal research notes, external broker research, and regulatory filings in a single interface

- Returns synthesised answers with citations linking back to source documents

- Surfaces prior internal coverage that an analyst would not have known to search for

- Operates as an assistant on a curated corpus, in line with the deployment pattern Morgan Stanley has publicly documented for its 100,000-document wealth management assistant, which now sees over 98 percent adoption among advisor teams

Business impact: Research time shifts from collection to interpretation. Senior analysts cover more situations with the same headcount, and the firm’s institutional research becomes a compounding asset rather than a buried archive.

Who it’s for: Asset managers, investment banks, hedge funds, and any institution where research synthesis is a core analyst function.

10. Pitch book and investment memo generation

What it is: Generative AI drafts the structural sections of each pitch book (market overview, transaction comps, company profile, valuation framework) from the bank’s internal data, leaving the banker to refine the narrative and the recommendations.

How generative AI enables it: Pitch books draw on standard templates, market data, comparable transactions, and company-specific information that is mostly available in the bank’s existing systems but has to be assembled by hand. The model handles the assembly; the banker handles the judgement.

Key capabilities:

- Generates the market overview section from internal research and external data sources

- Pulls transaction comparables from the bank’s deal database and formats them to the standard template

- Drafts the company profile and valuation framework from financial data and comparable benchmarks

- Built on custom AI software development anchored to the bank’s deal databases and template library

Business impact: Pitch book production is fundamentally constrained by analyst capacity. Removing the assembly burden compounds quickly across a deal team, and the time saved goes back into client conversations and bid preparation.

Who it’s for: Investment banks, M&A advisors, equity capital markets and debt capital markets teams, and any institution producing high volumes of pitch material.

11. Trading desk research synthesis

What it is: A trading desk synthesis tool that monitors news, regulatory updates, central bank commentary, and macroeconomic data continuously and generates concise briefings tied to the desk’s positioning within minutes of publication.

How generative AI enables it: The trading desk operates on a faster cycle than the research desk. The agentic pattern (autonomous monitoring with relevance-based push) delivers material that arrives in minutes, not hours, removing the lag between event and synthesis.

Key capabilities:

- Monitors central bank statements, news, and regulatory updates continuously across multiple languages

- Generates concise briefings flagging the differences from prior communications and any market-moving language

- Pushes briefings to the desk based on relevance rather than waiting to be asked, using agentic AI patterns

- Tracks which briefings actually drove trader actions, refining the relevance model over time

Business impact: On trading desks, latency between event and synthesis is competitive advantage. Compressing that latency from minutes-to-hours to seconds-to-minutes meaningfully changes the desk’s ability to act before competitors do.

Who it’s for: Sales and trading desks at investment banks, proprietary trading firms, hedge funds, and any institution where time-sensitive market synthesis drives PnL.

Insurance

Insurance is structurally information-heavy. Underwriting, claims, customer service, and regulatory reporting all run on documents that traditional automation could not read. According to Deloitte’s June 2024 survey of 200 US insurance executives, 76 percent of insurers have already implemented generative AI in one or more business functions, with life and annuity carriers slightly ahead of property and casualty insurers (82 percent versus 70 percent).

| # | Use Case | Core Problem | Technical Approach | Who It’s For |

|---|---|---|---|---|

| 12 | Underwriting automation and risk assessment | Slow submission triage, document-heavy analysis | LLM extraction and summary on submissions | P&C, life and annuity, commercial insurers |

| 13 | Claims processing and FNOL automation | Administrative load on claims handling | LLM document handling and adjuster case prep | All insurance carriers |

| 14 | Policy document generation and personalization | Dense policy docs customers don’t read | LLM-generated plain-language summaries | All carriers, especially regulated lines |

| 15 | Customer service and policyholder support | High-volume document-heavy customer queries | Conversational AI on policy, claim, and billing systems | All insurance carriers |

12. Underwriting automation and risk assessment

What it is: Generative AI compresses the submission triage and analysis cycle in commercial and specialty insurance lines by reading inbound submissions, extracting the risk data, cross-referencing against the carrier’s risk appetite, and generating a structured underwriting summary.

How generative AI enables it: Submission-to-quote times in many commercial lines are measured in days or weeks because the inbound data is messy and spans dozens of sources (loss runs, financial statements, broker submissions, third-party data, prior inspection reports). The model handles the document work; the underwriter focuses on judgement-intensive risks.

Key capabilities:

- Extracts risk data from broker submissions, loss runs, and supporting financial statements

- Cross-references each submission against prior similar risks and the carrier’s stated risk appetite

- Generates a structured underwriting summary that flags the points requiring underwriter attention

- Keeps pricing models and the actual risk decision under the carrier’s existing model risk framework

Business impact: Submission throughput rises while underwriter capacity is reallocated to higher-complexity risks. Speed-to-quote becomes a competitive differentiator without requiring additional underwriting headcount.

Who it’s for: Property and casualty insurers, life and annuity carriers, commercial and specialty lines insurers, and reinsurers.

13. Claims processing and FNOL automation

What it is: Generative AI automates the document layer of claims handling. It reads first notice of loss details, classifies the claim, requests missing documents in natural language, extracts data from incoming PDFs (police reports, medical records, repair estimates), and drafts the adjuster’s case summary.

How generative AI enables it: Most of the FNOL-to-resolution workflow is administrative: requesting documents, validating information, routing to the right adjuster. The model handles that layer end-to-end, while the adjuster owns the judgement on claim validity and disposition.

Key capabilities:

- Classifies inbound claims on first notice and routes to the appropriate adjuster queue

- Requests missing documentation from the policyholder in natural-language communication

- Extracts structured data from incoming PDFs (police reports, medical records, repair estimates) into the claims system

- Drafts the adjuster’s case summary so the file is ready for review rather than requiring assembly

Business impact: Claims cycle time is a primary driver of customer satisfaction in insurance, and administrative load is a primary driver of claims cost. Compressing both at once is one of the highest-ROI deployments available to a carrier.

Who it’s for: All insurance carriers, especially P&C and health insurers running high-volume claims operations.

14. Policy document generation and personalization

What it is: Generative AI reads the underlying policy data and generates plain-language summaries tailored to each customer: what is covered, what is not, what the deductibles and limits are, and what the customer needs to do at claim time. The legal policy document stays as the authoritative version.

How generative AI enables it: Insurance policies are dense, technical documents that customers rarely read and rarely understand. Producing personalised, customer-readable versions of every policy has historically been cost-prohibitive. Generative AI changes that calculus by generating the customer-facing layer from policy data.

Key capabilities:

- Generates plain-language policy summaries tailored to each customer’s specific coverage

- References back to the authoritative legal policy document section by section

- Updates summaries automatically when the underlying policy is amended

- Built on a machine learning and document workflow stack rather than a generic chatbot wrapper

Business impact: Policyholder comprehension improves, which reduces claim disputes and customer service volume. For carriers facing regulatory pressure on policyholder transparency, this is one of the higher-impact deployments available without changing the underlying policy framework.

Who it’s for: All insurance carriers, especially those operating in jurisdictions with active regulatory focus on policyholder transparency.

15. Customer service and policyholder support

What it is: A policyholder assistant that connects to the policy administration system, claim file, and billing record via API and resolves routine queries (policy questions, billing inquiries, claim status, document requests) without human escalation.

How generative AI enables it: Insurance customer service shares the call-volume characteristics of retail banking but with a heavier document burden: every interaction touches the policy, the claim file, or the billing record. The assistant reads all three sources together and answers the question with full context.

Key capabilities:

- Connects to policy administration, claims, and billing systems via API for real-time answers

- Applies the right jurisdictional rules based on the policyholder’s state or country of residence

- Cites the underlying policy document section for every coverage-related answer

- Built on a custom conversational AI stack rather than a SaaS chatbot adapted for insurance

Business impact: Contact centre cost compresses while customer satisfaction rises because answers arrive immediately rather than after callbacks. The second-turn experience is where horizontal SaaS chatbots typically fail, and where custom builds materially outperform.

Who it’s for: All insurance carriers, especially direct-to-consumer carriers and those with high policyholder service volumes.

Payments, Fintech, and Digital Assets

Payments and fintech have the smallest legacy burden and the fastest deployment cycles in financial services. They are also the first to see fraud and compliance issues at scale, which is where generative AI is delivering the most operationally visible value.

PwC’s research on generative AI in banking and financial services identifies five adoption stages, with most financial institutions today building initial use cases (private LLM applications, customer service and sales solutions, software development workflows) before scaling AI into broader operational workflows.

| # | Use Case | Core Problem | Technical Approach | Who It’s For |

|---|---|---|---|---|

| 16 | Fraud detection narrative and case investigation | Manual case file assembly | LLM case assembly and narrative drafting | Payment processors, card issuers, banks |

| 17 | Embedded finance and conversational commerce | Friction in non-financial customer journeys | Conversational AI at the point of sale | Embedded finance providers, fintechs |

| 18 | Crypto and digital asset compliance reporting | High-volume compliance documentation | LLM-generated SAR, KYC, and tax reporting | Crypto exchanges, digital asset platforms |

16. Fraud detection narrative and case investigation

What it is: When the fraud model flags a transaction, the AI assistant assembles the case file (transaction history, device data, location signals, prior cases involving similar patterns, related correspondence) and drafts the initial investigation narrative for the analyst’s review.

How generative AI enables it: Fraud detection itself has been a machine learning problem for two decades. What generative AI changes is the investigation and documentation layer that sits around the model. The analyst still makes the decision; the AI removes the case preparation work that previously consumed the bulk of investigation time.

Key capabilities:

- Assembles the case file across transaction systems, device data, and prior cases on the same pattern

- Drafts the initial investigation narrative explaining the model’s reasoning and the relevant signals

- Surfaces related correspondence (customer service interactions, prior disputes) that may inform the decision

- Generates the SAR narrative if escalation to financial crime is required, with citations to the underlying evidence

Business impact: Case handling throughput rises significantly without adding analyst headcount. Faster resolution translates to fewer false positives blocking legitimate transactions and better SAR documentation when escalation is needed.

Who it’s for: Payment processors, card issuers, retail and commercial banks, and any institution running active fraud and AML operations.

17. Embedded finance and conversational commerce

What it is: Generative AI handles the customer-facing conversational layer inside non-financial customer journeys: answering BNPL questions at checkout, walking small business customers through lending eligibility inside an accounting platform, supporting insurance purchase decisions at the point of product sale.

How generative AI enables it: Embedded finance requires the financial product to feel native to the originating platform. Generative AI is the layer that makes that conversation work in context, without the customer leaving the workflow they were already in.

Key capabilities:

- Answers customer questions about repayment terms, eligibility, and product mechanics in natural language

- Maintains conversation context across the customer’s journey on the host platform

- Surfaces regulatory disclosures at the right moments without breaking the user experience

- Built on agentic AI frameworks and standard AI integration patterns for connecting the financial backend to the third-party platform

Business impact: Conversion at the embedded touchpoint rises materially when the conversation is contextual rather than redirecting the customer to a separate portal. For embedded finance providers, this is the difference between a partnership that scales and one that stalls.

Who it’s for: Embedded finance providers, BNPL operators, fintechs powering banking-as-a-service, and traditional financial institutions building embedded distribution.

18. Crypto and digital asset compliance reporting

What it is: Generative AI compresses the documentation and reporting layer of digital asset compliance. It generates SAR narratives from underlying transaction data, drafts customer due diligence summaries from on-chain and off-chain sources, and produces tax reports that customers and regulators require.

How generative AI enables it: Digital asset platforms face a compliance burden that is heavier per transaction than traditional financial services, with KYC, source-of-funds verification, sanctions screening, suspicious activity monitoring, and tax reporting all happening at blockchain speed. The model handles narrative and documentation; the platform’s compliance engine handles detection and decisioning.

Key capabilities:

- Generates SAR narratives from underlying transaction data and detection model outputs

- Drafts customer due diligence summaries pulling from on-chain and off-chain identity sources

- Produces tax reports formatted to each jurisdiction’s specific requirements

- Built on custom AI software development because off-the-shelf tooling has not caught up with digital asset regulatory expectations

Business impact: Compliance cost scales linearly with transaction volume in traditional tooling. AI breaks that linear scaling, which is essential for any digital asset platform operating at scale.

Who it’s for: Crypto exchanges, digital asset custodians, stablecoin issuers, and any platform handling regulated digital asset activity.

Cross-Cutting: Risk, Compliance, and Operations

Some use cases apply across every subsector. AML, KYC, regulatory change tracking, and policy management are common to every financial institution operating today, and the AI deployment pattern is broadly similar regardless of subsector.

The IIF and EY’s 2024 survey on AI/ML use in financial services identifies risk, fraud, operations, and compliance as the four functions with the most predictive AI deployment across surveyed institutions, with generative AI now being layered on top of these established workflows.

| # | Use Case | Core Problem | Technical Approach | Who It’s For |

|---|---|---|---|---|

| 19 | AML/KYC document analysis and SAR drafting | High-volume compliance documentation | LLM document handling and narrative drafting | All financial institutions |

| 20 | Regulatory change management and policy automation | Constant regulatory change tracking | LLM monitoring and impact assessment on regulatory corpus | All financial institutions |

19. AML/KYC document analysis and SAR drafting

What it is: Generative AI compresses the document handling and narrative drafting layer of AML/KYC work. On onboarding, it reads the customer’s documentation and drafts the customer due diligence summary. On suspicious activity monitoring, it assembles the case context and drafts the SAR narrative for the compliance officer’s review and approval.

How generative AI enables it: AML/KYC is one of the most document-intensive compliance functions in financial services, and most of the work historically has been narrative writing on top of structured data. The model handles the assembly and first-draft writing; the compliance officer owns the judgement and the final approval.

Key capabilities:

- Extracts KYC data from customer onboarding documentation and flags inconsistencies before the file reaches compliance review

- Drafts customer due diligence summaries pulling from internal and external data sources

- Assembles SAR case context and drafts the narrative explaining the suspicious activity pattern

- Generates the documentation trail regulators expect for both onboarding decisions and SAR filings

Business impact: Case throughput rises significantly in compliance operations where narrative writing was the throughput constraint. The compliance officer’s time shifts from drafting to reviewing, which is the higher-value step.

Who it’s for: Banks, broker-dealers, asset managers, insurers, crypto platforms, and any financial institution operating under AML obligations.

20. Regulatory change management and policy automation

What it is: Generative AI monitors the regulatory environment, identifies changes relevant to the institution’s products and operations, drafts impact assessments, and proposes updates to internal policies and procedures.

How generative AI enables it: Every financial institution operates under a regulatory framework that changes constantly. New rules, amendments, guidance letters, enforcement actions, and supervisory expectations arrive daily across multiple jurisdictions. The model handles the monitoring and first-draft analysis; the compliance team reviews and approves.

Key capabilities:

- Monitors regulatory sources across multiple jurisdictions and identifies changes material to the institution

- Drafts impact assessments mapping each change to the institution’s affected products and procedures

- Proposes specific updates to internal policies based on the institution’s existing policy library

- Built on a retrieval-augmented generation system over the regulatory corpus and internal policies, calibrated to the institution’s risk appetite

Business impact: Faster response to regulatory change, better consistency across the policy library, and fewer gaps where the institution’s procedures fall behind the regulation. For institutions facing active examination cycles, this is a meaningful audit-readiness improvement.

Who it’s for: All financial institutions operating across multiple jurisdictions or under active regulatory examination.

Deployment Considerations for Financial Services

Most generative AI failures in financial services trace back to the same handful of issues, none of which are about the model itself. The handful below cover what determines whether a use case scales from pilot to production.

Model risk and governance. Any model that influences a credit decision, a customer recommendation, or a trading action sits under the institution’s model risk management framework. That means documented model selection rationale, ongoing validation, performance monitoring, and human review on edge cases. The right architecture is the one that produces this documentation as a byproduct rather than requiring it to be retrofitted later.

Data residency and sovereignty. Financial institutions operating across jurisdictions face data residency obligations that determine where models can be deployed and what data can leave a region. For European customers, GDPR and the EU AI Act constrain how models are trained and where inference runs.

For institutions in markets with explicit data sovereignty requirements, the model and its supporting infrastructure may need to run inside a specific country’s borders. These constraints often rule out off-the-shelf cloud SaaS and favour custom deployments that the institution controls end-to-end.

Hallucination control. A hallucinated response in financial services can be a compliance breach. The architectural answer is grounding: the model retrieves from the institution’s authoritative content rather than generating from its training data, and outputs include citations back to the source documents. For higher-risk use cases, two-stage validation (model output plus rules-based check or second-model verification) is standard practice.

Integration depth. The use cases that deliver real value are integrated into core banking, policy admin, claims, CRM, and risk systems. They are not chat interfaces sitting on top of generic search. Integration depth is where custom development outperforms horizontal SaaS, and it is what determines whether the assistant is useful in the second turn of every conversation or only the first.

Auditability. Every AI-influenced decision needs an audit trail showing what data was used, what the model output was, who reviewed it, and what action was taken. This is not optional. It is the precondition for regulator engagement, internal audit, and any eventual examination. Building auditability into the architecture from the start is materially less expensive than retrofitting it later.

Develop AI Solutions Built for Regulated Financial Workflows

Space-O AI develops them as custom software anchored to your existing core systems, with audit trail and model risk documentation produced as a byproduct of the build, not retrofitted afterwards.

Why Financial Institutions Choose Space-O AI

Financial services generative AI is a different build problem than horizontal AI. The model is the easy part. The hard parts are governance documentation that survives examination, integration depth that holds up under load, and hallucination control on every output that touches a customer or a regulator. For the underlying technology context, our generative AI guide explains how LLMs and RAG handle document-intensive, compliance-heavy environments.

Space-O AI builds for this constraint set. Every engagement starts with the institution’s governance posture (what is the model risk management framework, what is the third-party risk process, what data can leave the institution’s environment), and the build sequence is structured around producing the audit trail as a byproduct rather than retrofitting it later. The use cases above are not theoretical for us. They are the work we are doing.

What changes when you build with us. Model selection is grounded in the institution’s actual risk tolerance and data residency requirements rather than defaulting to the loudest commercial model.

The evaluation framework is built before the first production deployment, so every model output is tested against the institution’s specific tolerance for accuracy, bias, and regulatory consistency. Integration with core banking, policy administration, claims, CRM, and risk systems is treated as the primary technical challenge, not an afterthought.

Audit trails, citation grounding, and human-in-the-loop controls are part of the architecture from day one. Our AI consulting practice sequences the build, and our AI integration work covers the architecture from data pipeline to model serving to audit trail.

Where most institutions should start. Document-heavy workflows with established regulatory frameworks: credit memos in commercial banking, KYC document analysis at onboarding, FNOL automation in insurance, and regulatory reporting assembly.

These three characteristics (high volume, document-heavy, regulated framework already understood) are what make a 90-day pilot realistic. Once one use case is live and the governance pattern is proven, the second and third deploy faster because the framework is already there.

Book a discovery call with Space-O AI to scope your first financial services AI deployment.

Frequently Asked Questions

Which financial services use cases are realistic to deploy in the next two quarters versus the next two years?

Near-term (90-180 days): KYC document analysis at onboarding, credit memo drafting for commercial banking, FNOL automation in insurance, regulatory reporting assembly, customer service assistants for retail banking. All have established regulatory frameworks, well-understood data sources, and clear success metrics.

Two-year horizon: autonomous credit decisioning, end-to-end claims automation, integrated wealth advisor copilots.

These require deeper model risk validation, additional regulatory engagement, and broader workflow change management before scaling.

How does generative AI fit inside an existing model risk management framework like SR 11-7?

Generative AI does not exempt itself from model risk requirements. The institution’s existing model risk framework still applies, with two additional considerations: hallucination as a model error category (handled through retrieval grounding and validation layers), and the model’s continuous evolution (handled through version control, change documentation, and re-validation triggers). The right architecture produces the model risk documentation, validation evidence, and monitoring outputs that the institution’s MRM function expects, rather than treating them as additional work.

Can generative AI be used for credit decisioning, fair lending, and underwriting?

The decision itself stays with the institution’s existing decisioning model and credit policy. Generative AI supports the workflow around the decision: drafting credit memos, generating adverse action notices in compliant language, summarising applications, surfacing comparable prior decisions, and producing the documentation regulators expect. For fair lending, the model handles the explanation layer (which factors drove the decision, in customer-readable language) without changing the underlying decision logic. This separation is what makes deployment viable under existing fair-lending and ECOA requirements.

What data can a generative AI system use, and what stays out?

Customer PII, transaction data, and confidential client information typically stay inside the institution’s environment, with the model running in a tenant or deployment the institution controls. Training data is curated from the institution’s own corpus rather than open-internet sources. For closed-source foundation models, contracts specify that customer data is not used to train the underlying model. For higher-risk deployments, open-source models running inside the institution’s own infrastructure are increasingly the preferred architecture because they remove the third-party data residency question entirely.

How is hallucination handled when an AI-generated output reaches a customer or a regulator?

Two architectural answers, layered. First, retrieval grounding: the model retrieves from the institution’s authoritative content (policy documents, regulatory text, customer files) rather than generating from its training data, and every output includes citations back to the source. Second, validation layers: for customer-facing or regulator-facing outputs, a second-pass check (rules-based, second-model verification, or human review) confirms the output before it ships. The threshold for which layer applies is set based on the consequence of an error: a customer service answer is a different risk tier than an adverse action notice or a SAR narrative.

What does the audit trail look like for a regulated generative AI deployment?

Every AI-influenced output produces a record covering: the input that triggered it, the data the model retrieved, the model’s output, any validation checks that ran, who reviewed it, what action was taken, and the timestamps for each step. The trail is queryable for examination on demand, exportable in the formats regulators expect, and retained according to the institution’s record management policy. Building this trail into the architecture from day one is materially cheaper than reconstructing it later.

Build, buy, or partner: what is the right path for a financial institution starting generative AI?

For non-differentiating use cases where the institution’s data is not a competitive moat (basic content generation, internal knowledge search, IT productivity), commercial tools are usually the right answer. For use cases where the institution’s data, customer relationships, regulatory posture, or workflow specifics are competitive (customer-facing assistants, credit memo drafting, claims processing, KYC, regulatory reporting), custom builds anchored to the institution’s actual systems materially outperform horizontal SaaS. The architectural depth that custom development provides (integration, governance, hallucination control, audit trail) is also what regulators expect to see on examination.